Public Policy · Municipal Finance

Toronto's Fiscal Future: The Case for Structural Reform

A submission to the City of Toronto Budget Committee — January 2026. The 2026 budget is technically competent. It is also insufficient. Here is why, and what an honest path forward looks like.

Toronto is one of the most economically productive cities in North America. It hosts the headquarters of major financial institutions, draws billions in foreign investment, and generates a disproportionate share of Ontario's GDP. And yet, year after year, its government returns to the same exhausted toolkit — incremental property tax increases, reserve draws, and deferred maintenance — to manage a structural fiscal challenge that those tools are constitutionally incapable of solving.

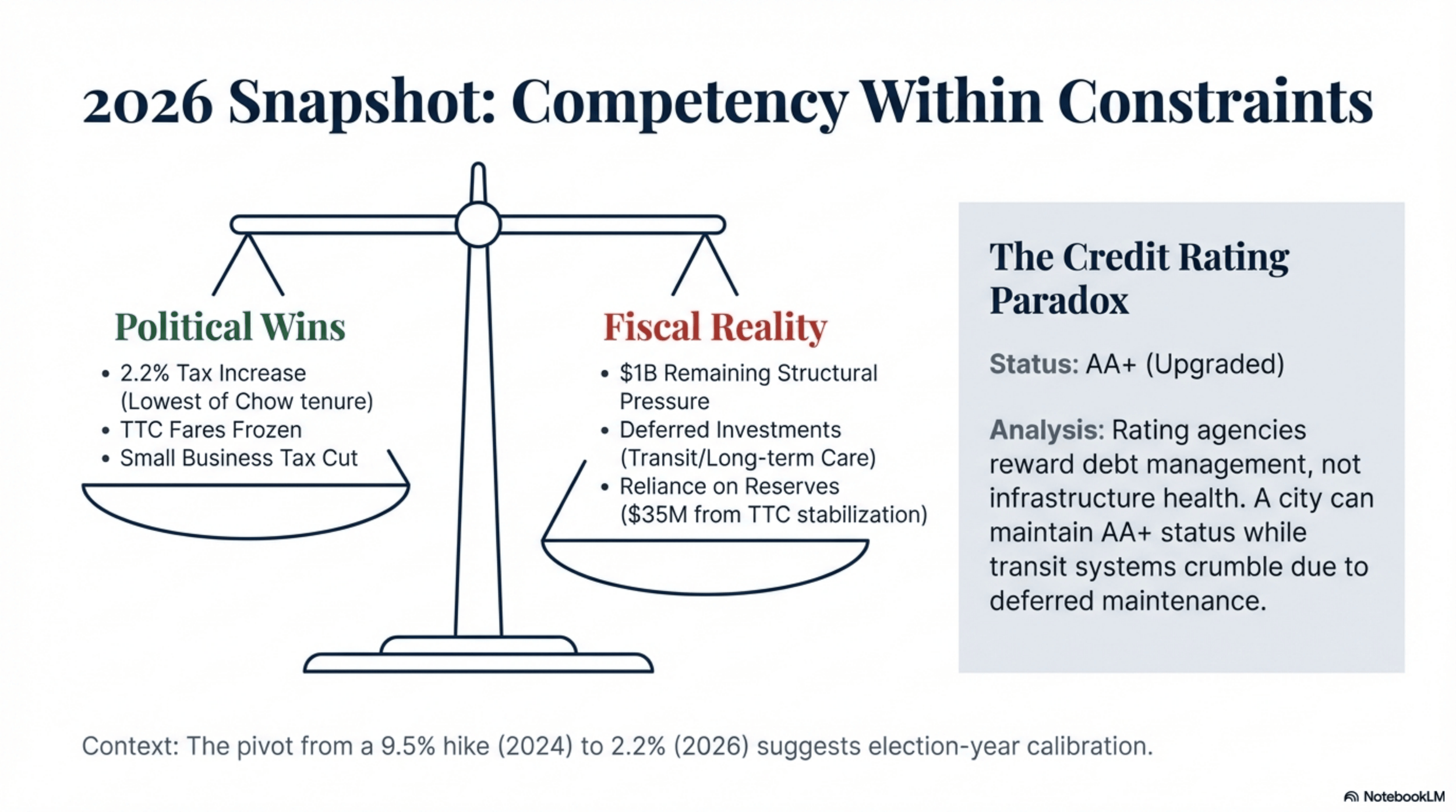

The 2026 operating budget is, in many respects, a competent document. It holds the property tax increase to 2.2 percent, freezes TTC fares, and delivers a small business tax reduction. These are genuine political achievements in a constrained environment. But the budget also leaves approximately one billion dollars in structural pressure unresolved, draws on reserves including thirty-five million dollars from TTC stabilization funds, and defers critical investments in transit and long-term care.

The credit rating agencies have upgraded Toronto to AA+ — a fact the administration has cited with justifiable satisfaction. What that rating reflects, however, is disciplined debt management, not infrastructure health. A city can maintain AA+ status while its transit systems deteriorate and its capital backlog grows. The rating tells you how the books are kept. It does not tell you whether the city is investing in its own future.

The core problem is structural, not managerial. Toronto cannot tax its way to fiscal sustainability on a 19th-century revenue base while funding a 21st-century city.

The Structural Trap

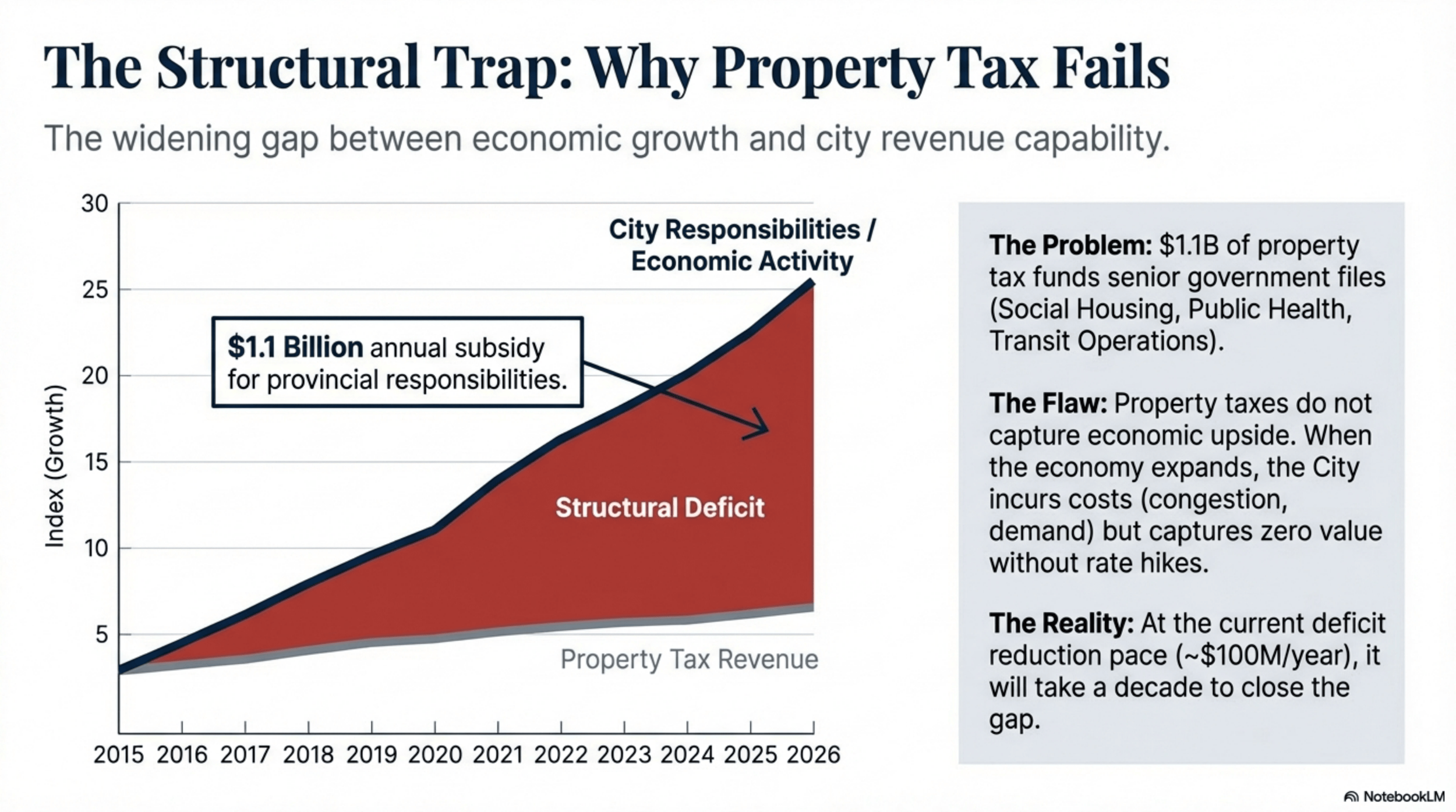

Toronto bears the costs of a senior government while retaining the revenue tools of a small town. The city spends approximately 1.1 billion dollars annually subsidizing provincial responsibilities — social housing, public health, transit operations — that other provinces fund directly. The property tax, Toronto's primary revenue instrument, is both constitutionally constrained and structurally inadequate: it does not grow with the economy, it cannot be restructured without provincial approval, and it is already among the highest in the Greater Toronto Area, limiting the city's competitive position relative to neighbouring municipalities.

The consequence is a structural deficit that compounds annually. The 2026 budget papers acknowledge it; they do not resolve it. Reserves are drawn down. Capital projects are deferred. The maintenance backlog grows. Each year's budget begins under greater pressure than the last, and each year's toolkit is the same one that failed to close the gap the year before.

Estimated annual Toronto expenditure subsidizing responsibilities that other provinces fund directly — social housing, public health, and transit operations that are not Toronto's constitutional obligation to carry alone.

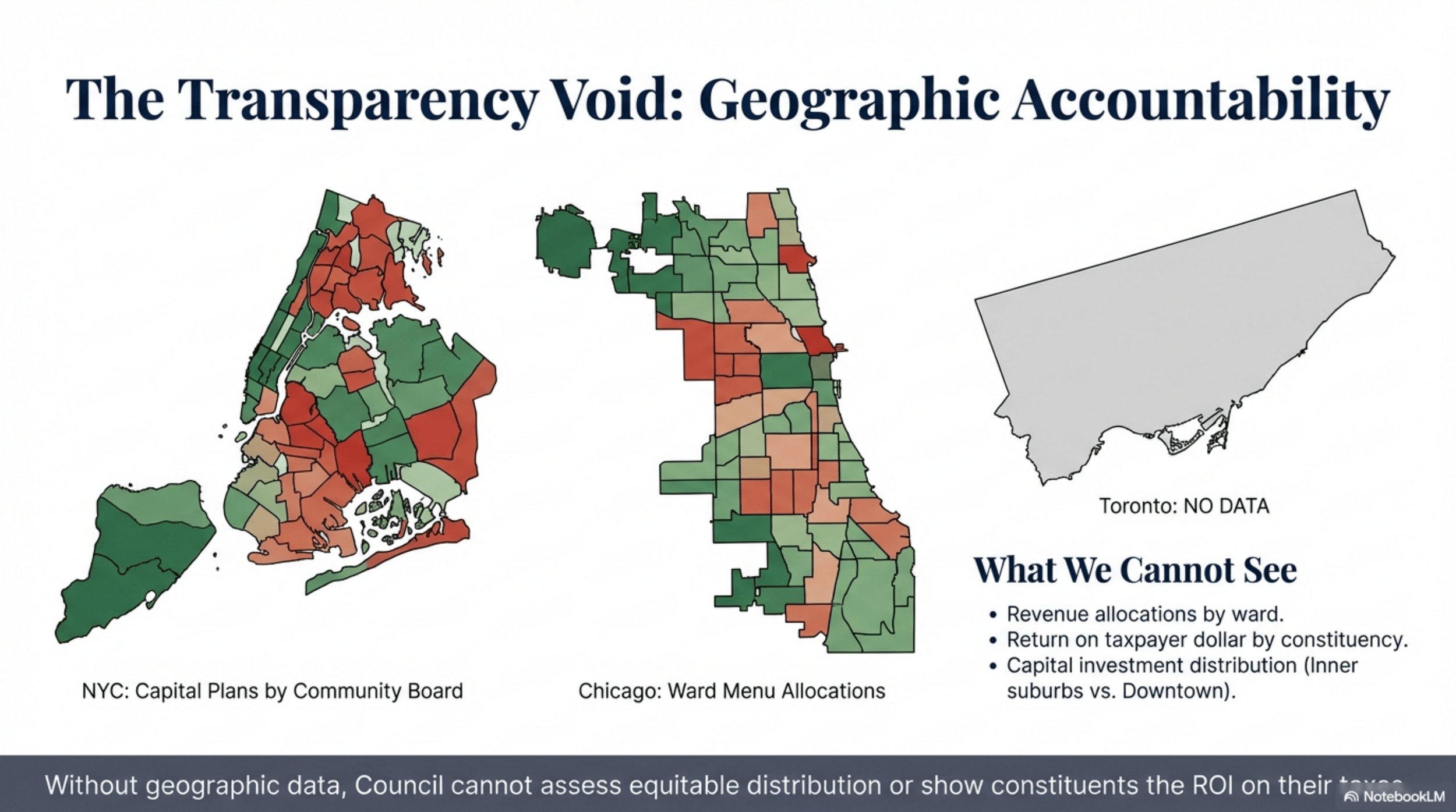

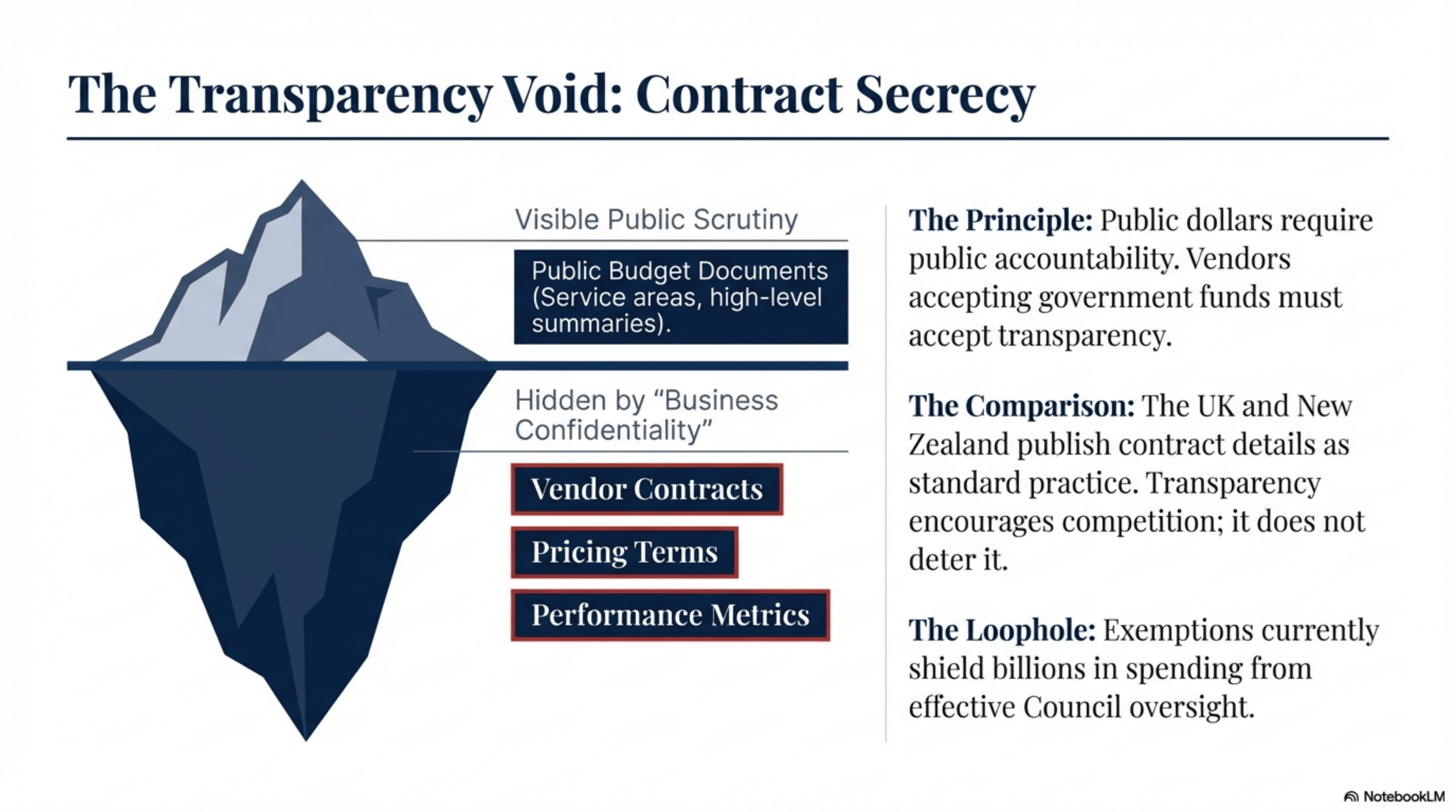

The Transparency Deficit

Before the city asks residents to accept new revenue tools, it owes them a clear accounting of how existing resources are deployed. Toronto's budget documents are voluminous. They are not, in any meaningful sense, transparent. Line-item accountability for major program areas is difficult to extract even for sophisticated analysts. Two dimensions of this transparency failure deserve particular attention.

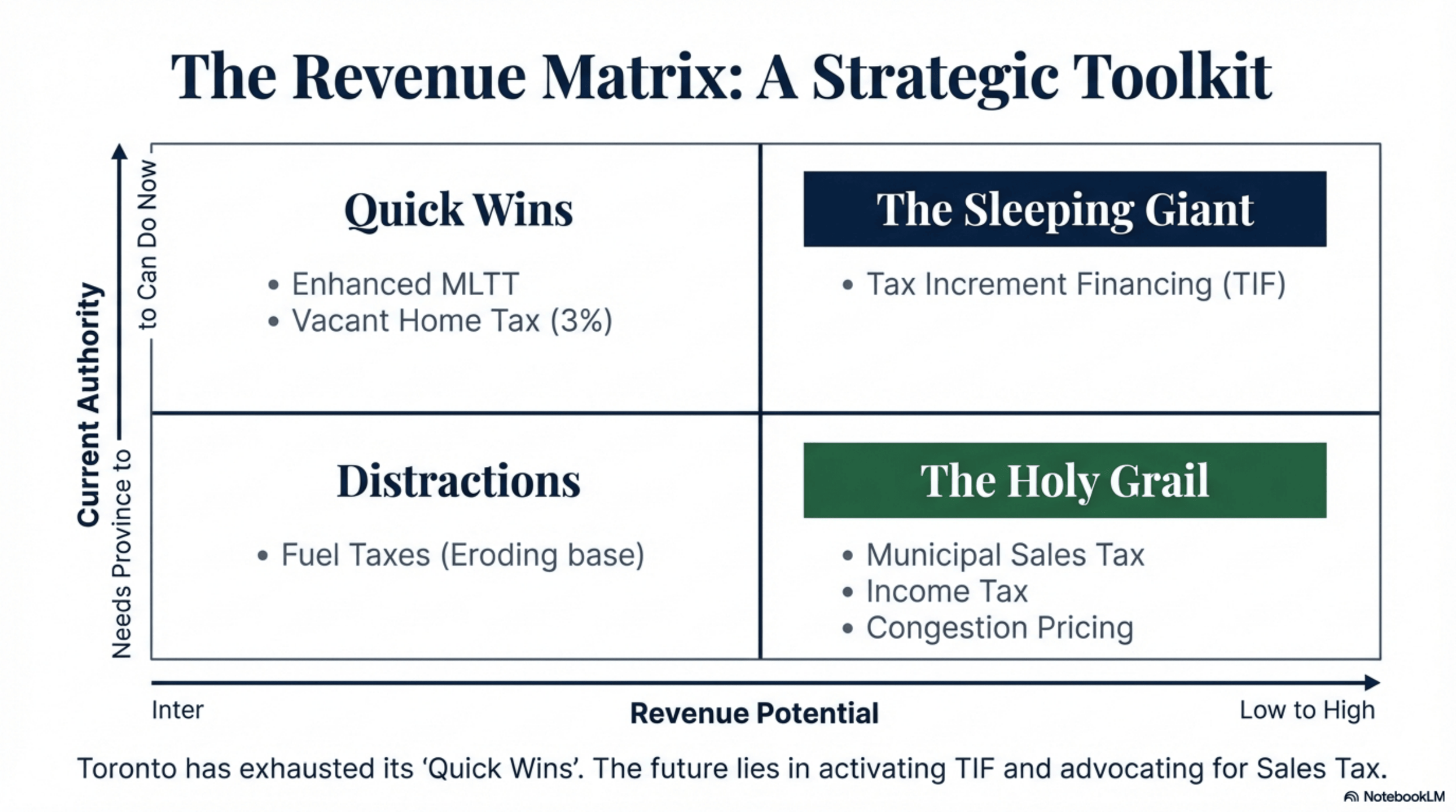

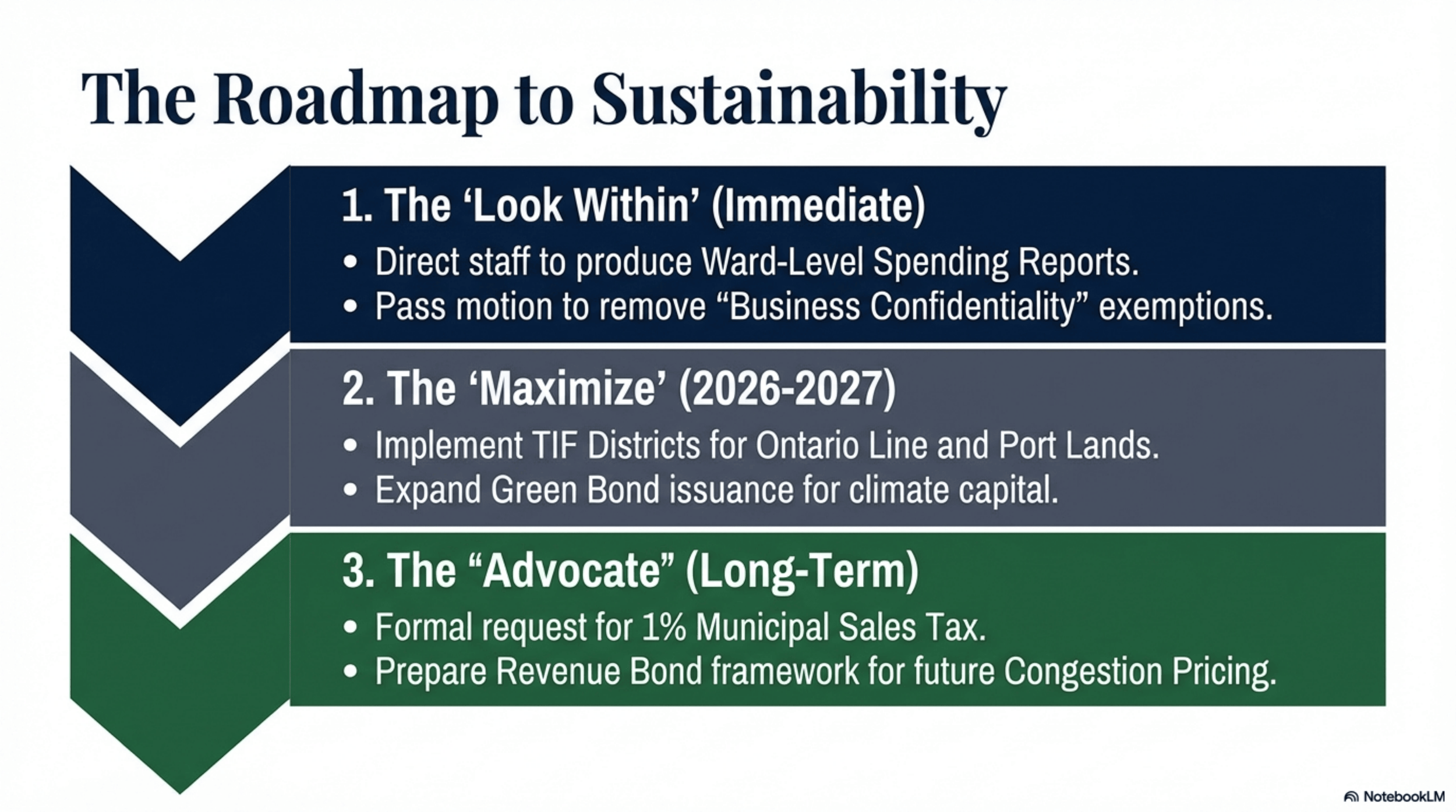

Three Tools the City Is Not Using

The presentation I made to the Budget Committee identified three revenue and financing instruments that are available, proven in comparable jurisdictions, and appropriate to Toronto's situation. None of them require constitutional amendment. None of them are exotic. All of them require political will that has, to date, been absent.

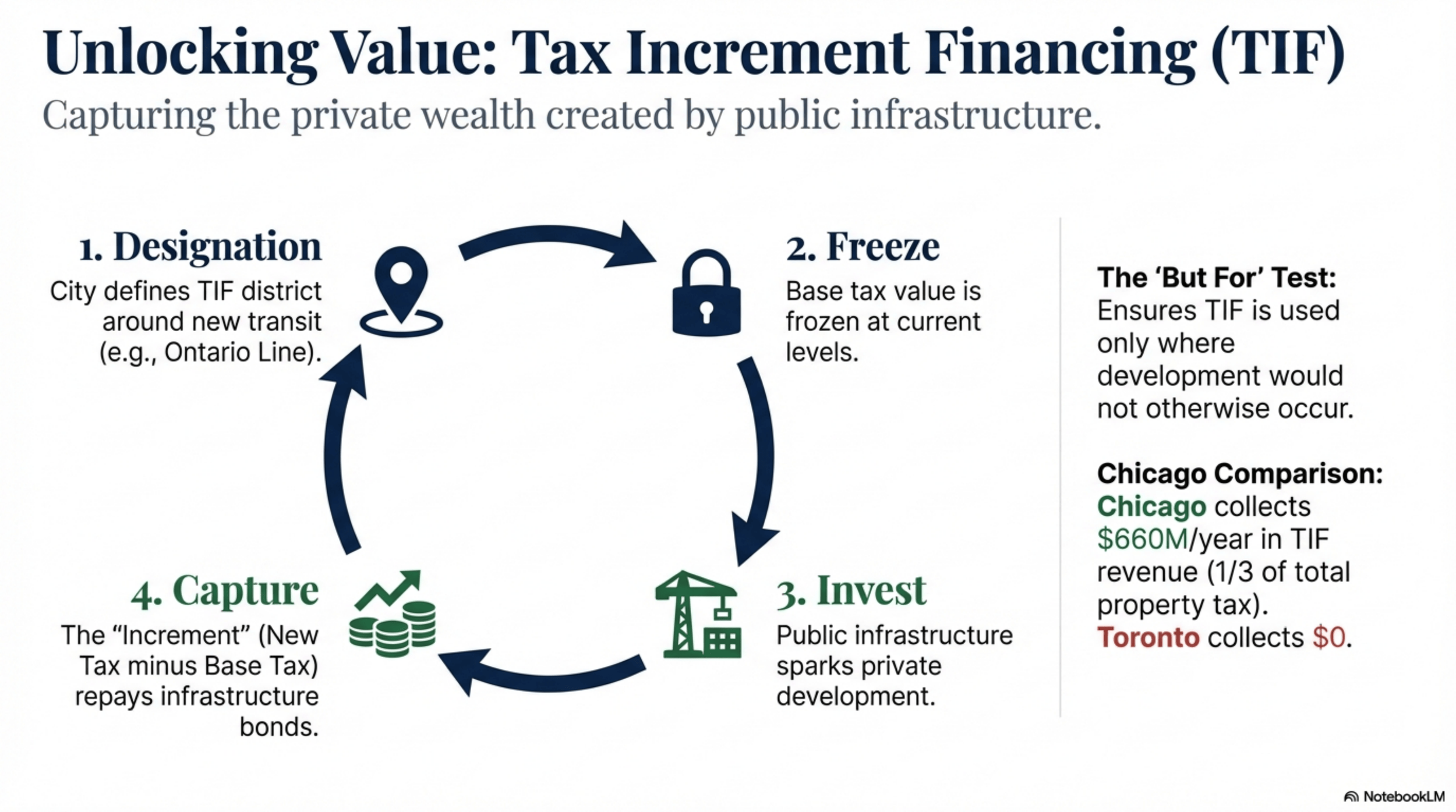

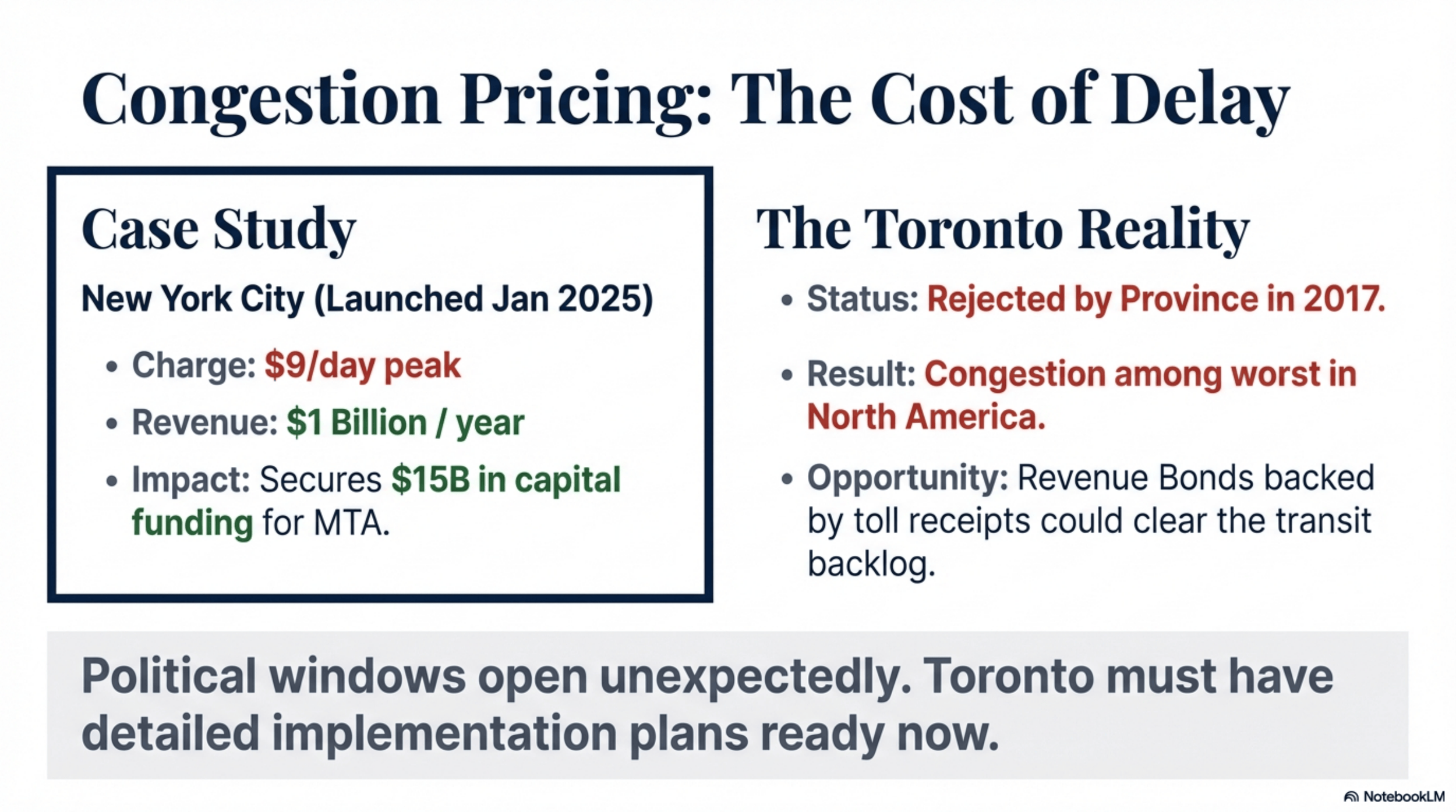

Tax Increment Financing (TIF). TIF is a development finance tool that captures the incremental property tax revenue generated by a defined improvement district and redirects it to fund the infrastructure investment that produced the increase in value. It is in routine use in Chicago, Denver, Portland, and dozens of other North American cities. Toronto has the statutory authority to implement TIF under the Development Charges Act and related provincial legislation. It has not done so at meaningful scale. A well-structured TIF framework targeted at transit-adjacent development corridors could generate hundreds of millions in non-tax financing over a twenty-year horizon without requiring a single additional dollar from the operating budget.

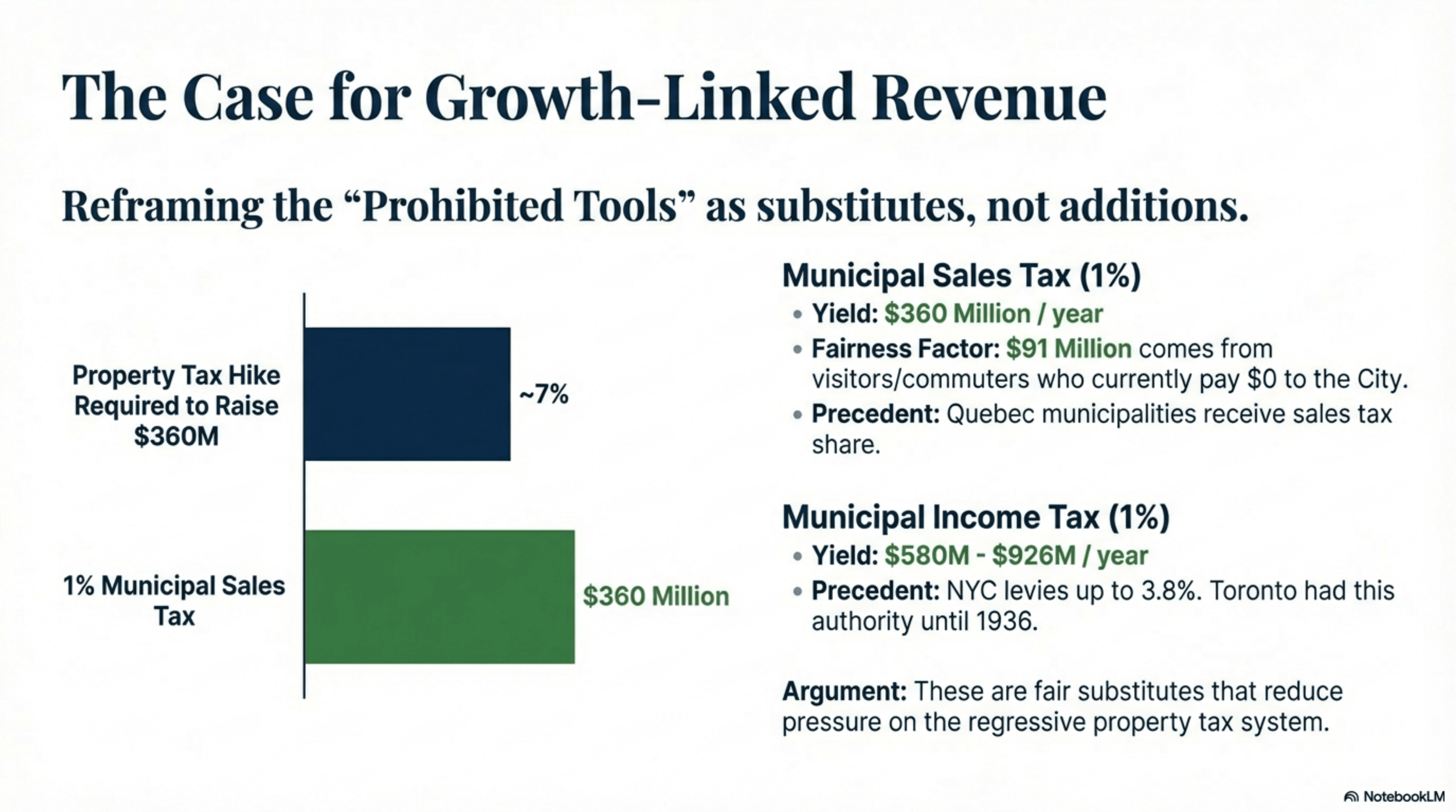

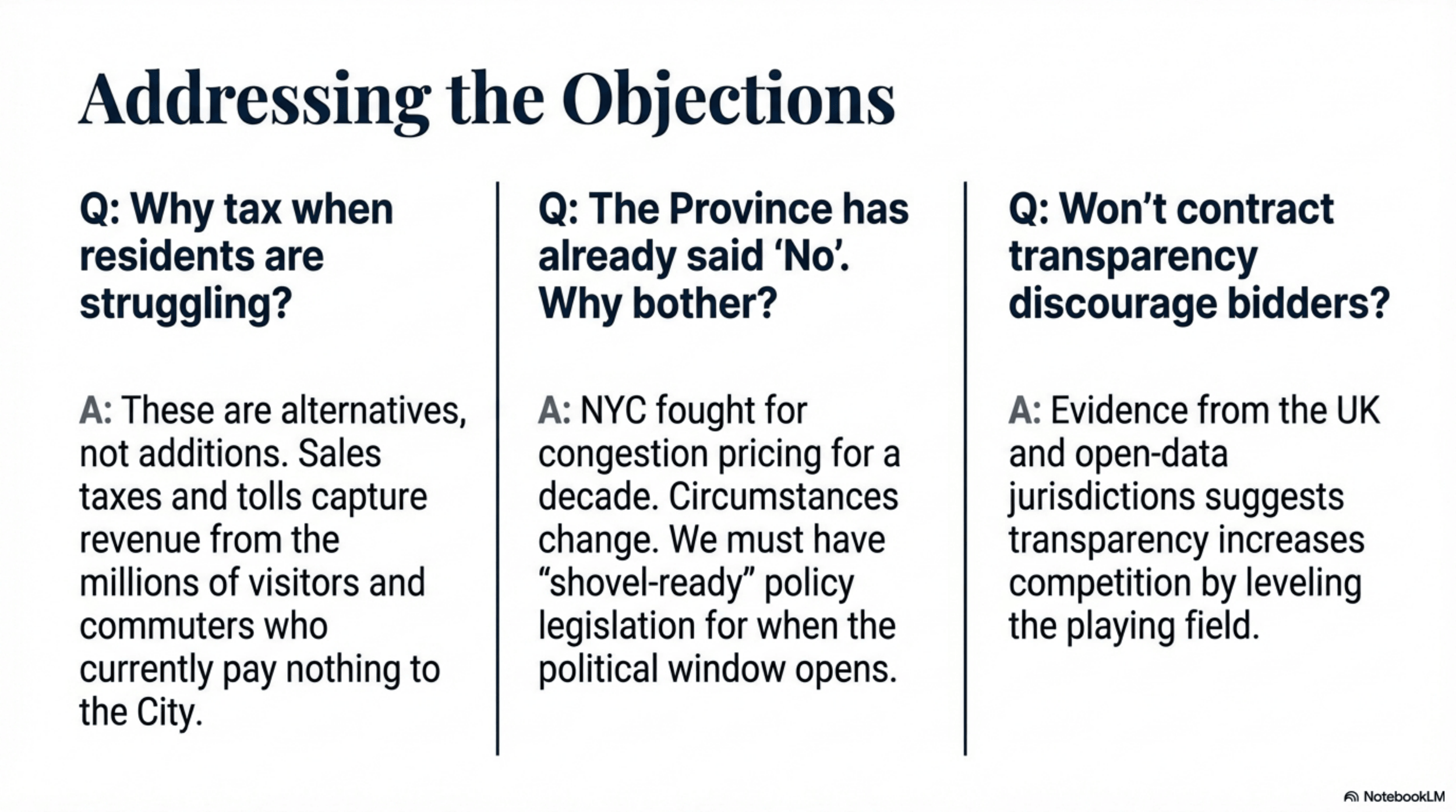

A Municipal Sales Tax. The City of Toronto Act grants Toronto broader fiscal authority than any other Ontario municipality. That authority has been underutilized. But, more importantly, critical growth-based taxation has not been a part of the puzzle. A modest municipal sales tax — in the range of one percent — would generate an estimated 360 million dollars annually, diversify the city's revenue base away from property values alone, and align Toronto's fiscal architecture more closely with major North American peer cities. The objection that such a tax would disadvantage Toronto relative to surrounding municipalities is legitimate but manageable: it argues for a thoughtfully phased implementation and regional conversation, not for indefinite inaction. A perhaps preferable alternative is a one percent income tax - more progressive - meaning that those able to pay more pay more. In either case, provincial authorization is required and to date has not been forthcoming. The City needs to be relentless in advancing arguments for broader taxation powers.

Estimated annual revenue from a one-percent municipal sales tax — enough to close a significant portion of the structural gap without touching property tax rates or drawing down reserves.

Genuine Spending Transparency. The third tool is not a revenue measure. It is a governance measure, and it matters as much as the first two. Before the city asks residents to accept new revenue tools, it owes them a clear accounting of how existing resources are deployed. A zero-based review of the largest program budgets, published in plain language with meaningful benchmarks against comparable cities, is the foundation on which public trust in new fiscal measures must be built.

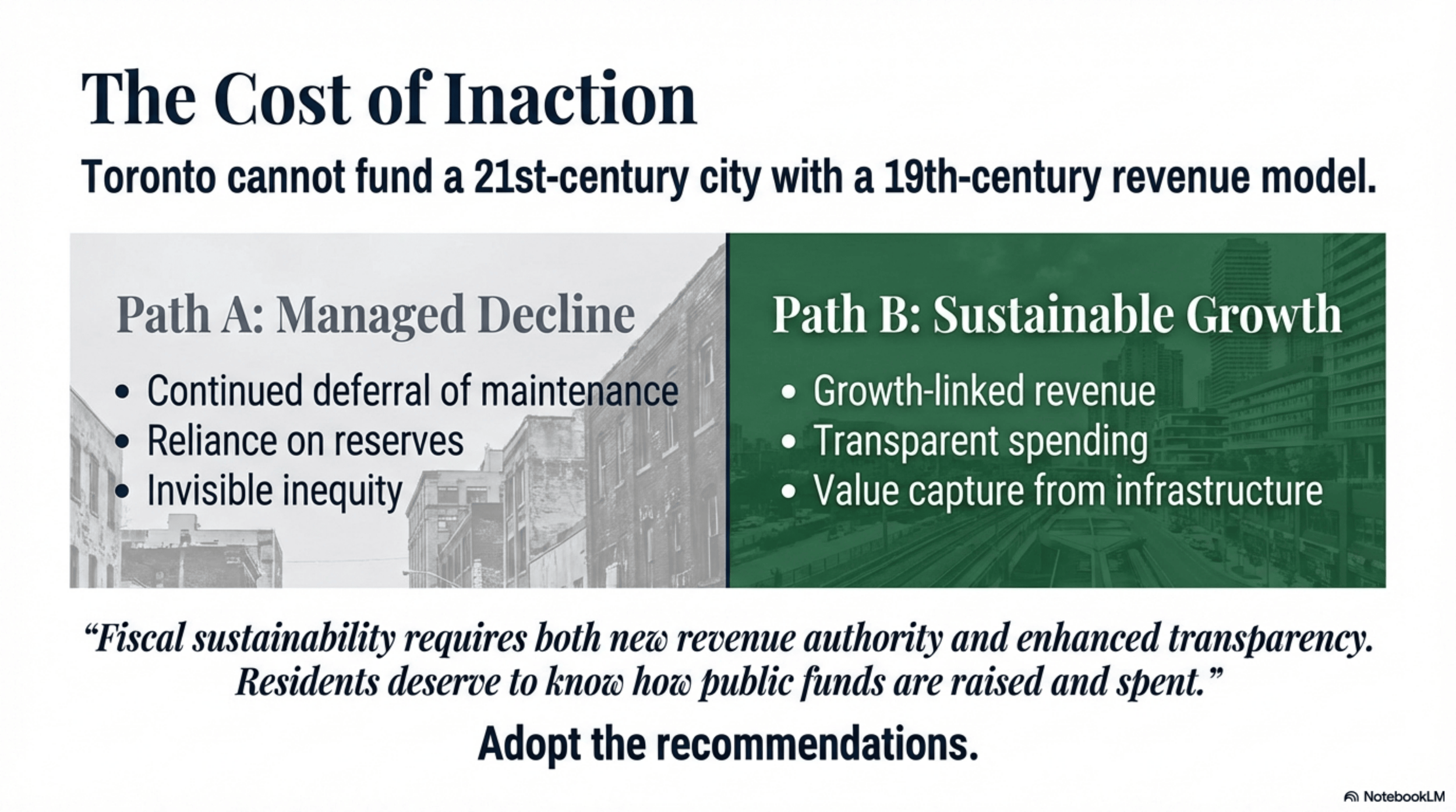

Two Paths

The city has, in practical terms, two paths available to it.

Path A — Continuation

Incremental management of a structural problem

- Annual property tax increases of 2–4%

- Continued reserve draws

- Deferred capital investment

- Growing maintenance backlog

- Structural gap unchanged or widening

- Credit rating preserved; service quality declining

Path B — Structural Reform

New tools for a new fiscal architecture

- TIF framework for transit-adjacent corridors

- Municipal sales tax — phased and regionally coordinated

- Zero-based spending review with public reporting

- Provincial negotiation on shared-cost responsibilities

- Structural gap reduced; investment capacity restored

Path A is politically easier in the short term. It is fiscally irresponsible over any meaningful planning horizon. The infrastructure deficit that accumulates under Path A does not disappear — it compounds, and it eventually presents itself as an emergency capital requirement that is far more costly to address than the incremental investment that would have prevented it.

Path B requires political courage. It requires the city to have a frank conversation with its residents about what a world-class city costs and what revenue tools are appropriate to fund it. It requires engagement with the province on the appropriate allocation of social service costs. None of these are comfortable conversations. All of them are necessary ones.

The question before the Budget Committee is not whether the structural problem can be deferred again. It can. The question is how much deferral will cost, and who will pay for it.

A Note on the Provincial Relationship

No analysis of Toronto's fiscal position is complete without acknowledging the provincial dimension. The City of Toronto Act's broader fiscal authority exists on paper. In practice, the city's relationship with Queen's Park has, for most of the past decade, been one of dependency rather than partnership. Provincial decisions — on transit funding allocation, on development charge rules, on the uploading or downloading of program costs — have material consequences for Toronto's budget that the city can neither predict nor control with precision.

A mature fiscal strategy for Toronto must include a sustained, evidence-based advocacy effort directed at the province: for the uploading of provincial program costs that Toronto currently carries, for a revised funding formula for transit operations, and for the regulatory flexibility to implement the revenue tools the City of Toronto Act nominally permits. This is not a political ask. It is a governance ask, grounded in comparative evidence about how other major cities in federal systems manage the relationship between municipal and senior government fiscal responsibilities.

Conclusion

The 2026 budget is not a failure. It reflects competent management of an inherited structural problem within a constrained set of tools. What it does not do — what no incrementally-managed budget can do — is resolve the underlying mismatch between Toronto's responsibilities and its revenue architecture.

The tools to address that mismatch exist. They have been used successfully in comparable jurisdictions. They are available to Toronto under existing statutory authority, subject to political will and, in some cases, provincial engagement. The city's residents deserve a frank accounting of why those tools have not been deployed, and a credible plan for deploying them.

That is the conversation the Budget Committee should be having. This submission is an attempt to start it.

Darrell Brown is a senior Ontario barrister and strategic advisor. He has practiced before all levels of court including the Supreme Court of Canada, and has provided government relations counsel producing legislative and regulatory outcomes at federal, provincial, and municipal levels over several decades. This article is adapted from remarks delivered to the City of Toronto Budget Committee, January 2026.